- Markets

Find out what influences market movements by browsing through our tailor made product pages.

- Trading Platforms

Maximise your investment opportunities

Trading Platforms

In order to ensure our customers have the best trading experience. We are proud to introduce our suite of trading platforms.

- Accounts

All accounts can be opened using one application form.

OPEN A LIVE ACCOUNT

The application process is simple and straightforward. You can complete the online application form and be trading in minutes.

- Academy

Here you will find all the details regarding One Financial Markets educational offering

TRADING ACADEMY

Working through each of our six online modules, detailed below, you can develop your trading confidence

- Newsroom

The latest news in the Financial Markets from across the globe.

LATEST NEWS

Make sure you don't miss out on what's going on in the world around you, keep up to date with our market commentary and daily market update videos.

- Contact Us

NTPC's Q4 Performance and Strategic Developments: Goldman Sachs Analysis

Goldman Sachs (NYSE:GS) has analyzed NTPC’s fourth-quarter performance for FY24, noting an adjusted consolidated profit after tax (PAT) of Rs 53 billion, slightly below the estimated INR 55 billion. This shortfall was due to higher-than-expected fixed cost under-recovery from operational issues at the Barh and Barauni power plants.

NTPC’s renewable energy portfolio has expanded to 23.2 GW at various development stages. The management plans to monetize this growth through an Initial Public Offering (IPO) by October-November 2024. Post-monetization, NTPC (NS:NTPC) will continue to support the renewable segment's growth if needed. The completion of these renewable projects is expected by FY27.

Offer: You can get InvestingPro at a steep discount of up to 69%, for INR 216/month, for a very limited time. Investors are already taking advantage of such a mouth-watering price to ramp up their investing game. In case you are finally ready to up your investing journey, Click here before time runs out.

NTPC's new coal project pipeline stands at 15.2 GW, with over 10 GW expected to be ordered in FY25. Additionally, NTPC is entering the nuclear energy sector, planning to order the 2.8 GW Mahi Banswara nuclear power plant in partnership with the Nuclear Power Corporation of India within the current fiscal year. This move into nuclear energy is expected to ensure long-term growth stability for NTPC's core business after the renewable business monetization.

Goldman Sachs maintains a 'Buy' rating for NTPC, despite a recent share price rally. Analysts foresee the coal capacity pipeline growing by an additional 12 GW, enhancing the value from renewable business monetization. NTPC's stock is trading at a forward price-to-book value (P/BV) of 1.9x, which, despite being above its historical median, is still significantly lower than the 3.4-3.6x multiples of private sector peers like Tata Power (NS:TTPW) and JSW Energy (NS:JSWE).

NTPC’s strategic positioning in both thermal and renewable energy sectors is highlighted, with a stable regulated business model offering a 3% dividend yield, adding a margin of safety for investors. Goldman Sachs has adjusted its forecasts based on FY24 numbers, predicting a 15% compound annual growth rate (CAGR) in earnings for FY24-27, driven by a 7% CAGR in regulated equity, a 37% CAGR in joint venture profits, and early contributions from the renewable energy business.

Image Source: InvestingPro+

Goldman Sachs values NTPC at a target price of INR 395 per share, implying a FY26 estimated P/BV of 2x and an FY26 estimated enterprise value-to-EBITDA multiple of 12x for the renewable business, reflecting high growth potential and strategic options. Key risks include potential delays in new coal plant executions, aggressive renewable energy bidding, adverse movements in module prices or debt costs, and unfavorable regulatory changes.

Image Source: InvestingPro+

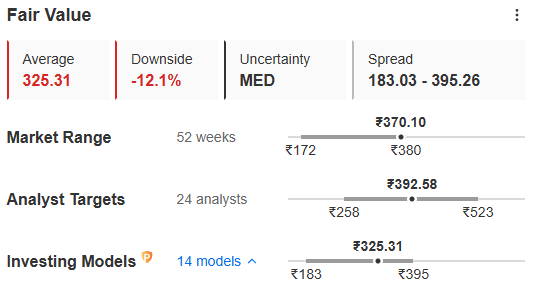

Even with InvestingPro’s financial models, the intrinsic value of INR 395 is an extreme end, the highest among 14 models. For a more realistic approach, the fair value is considered as the accurate metric for valuation as it takes a mean of all values which helps avoid extreme valuations. In this case, the fair value is 325, depicting a 12% downside potential from the MCP of INR 370.

Another thing to note is the stock has already run up 116% in the last one year, therefore waiting for the prices to cool down before going on the stock might be a better strategy.

Click here Subscribe to InvestingPro now at a discount of up to 69%, for just INR 216/month and unlock the full potential of your investments.

Also Read: Unveiling the Power of Fair Value with InvestingPro+

X (formerly, Twitter) - Aayush Khanna

Begin trading today! Create an account by completing our form

Privacy Notice

At One Financial Markets we are committed to safeguarding your privacy.

Please see our Privacy Policy for details about what information is collected from you and why it is collected. We do not sell your information or use it other than as described in the Policy.

Please note that it is in our legitimate business interest to send you certain marketing emails from time to time. However, if you would prefer not to receive these you can opt-out by ticking the box below.

Alternatively, you can use the unsubscribe link at the bottom of the Demo account confirmation email or any subsequent emails we send.

By completing the form and downloading the platform you agree with the use of your personal information as detailed in the Policy.